If Midland Credit Management has shown up on your credit report, sent you a letter, or called you about an old debt, stop everything before you do anything else.

Do not pay. Do not call them back. Not yet.

Before you make a single move, you need to understand exactly what Midland Credit Management is, what your legal rights are, and what options you actually have. Because the first move you make could either save you hundreds of dollars, or cost you thousands.

In this complete guide you will learn everything you need to know about Midland Credit Management, who they are, whether they are legit, what happens if they file a lawsuit against you, how to negotiate a settlement and exactly what to do right now.

We have already helped thousands of readers navigate debt collectors like Unifin, Portfolio Recovery Associates and LVNV Funding LLC. Today we are breaking down Midland Credit Management in the same complete, plain English way.

What Is Midland Credit Management?

Midland Credit Management, also known as MCM, is one of the largest debt collection companies in the United States. They are a subsidiary of Encore Capital Group, a publicly traded company on the NASDAQ stock exchange.

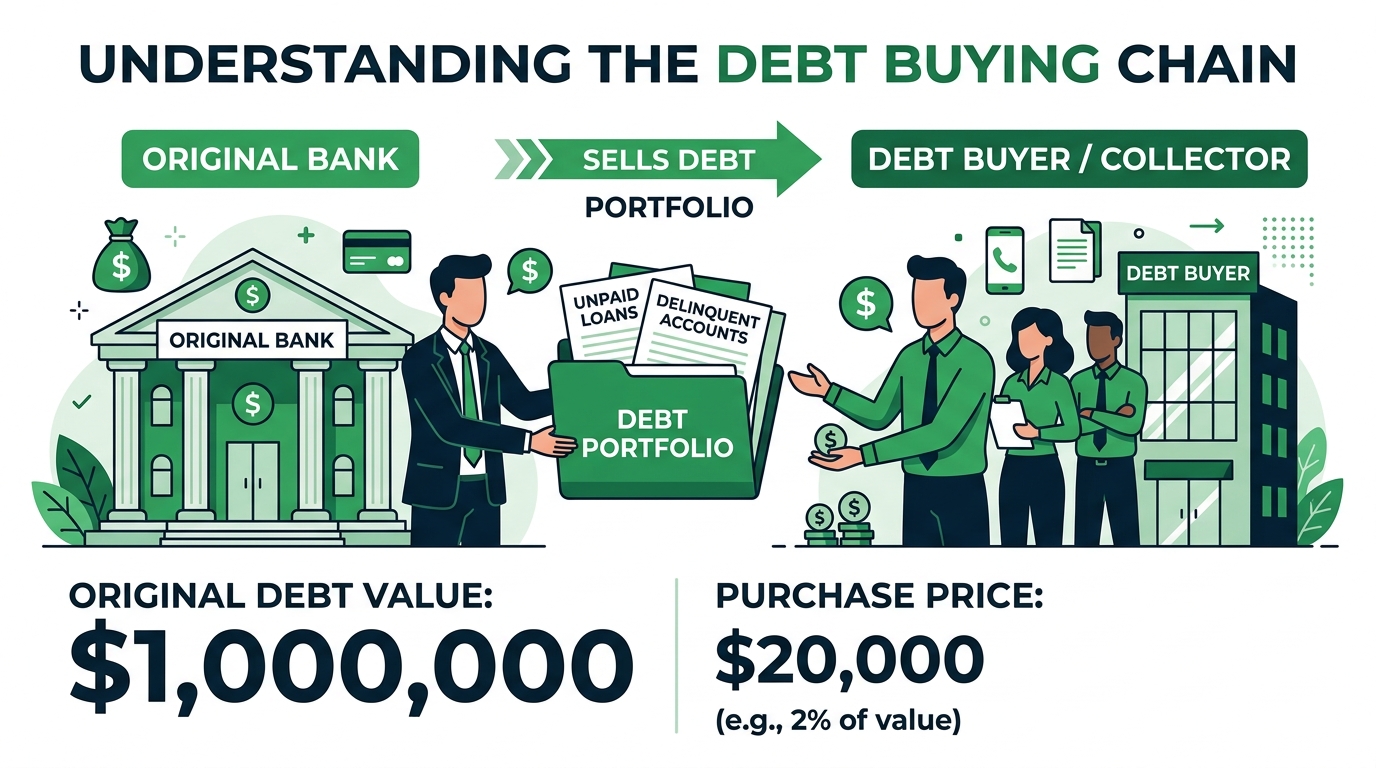

Midland Credit Management is what is known as a debt buyer. They do not represent your original lender. Instead they purchase large portfolios of old, unpaid debts from banks, credit card companies and other lenders for a tiny fraction of what those debts are worth.

Once Midland Credit Management purchases your debt they become the legal owner of it. They then attempt to collect the full original balance from you, even though they paid just pennies on the dollar to acquire it.

Midland Credit Management Inc is headquartered in San Diego, California and has been operating since 1953. They are one of the oldest and largest debt buyers in America with billions of dollars in purchased debt portfolios.

So is Midland Credit Management legit? Yes, absolutely. They are a real, regulated, legitimate company. But legitimate does not mean you have to pay them without doing your homework first. And it certainly does not mean they always play by the rules.

Is Midland Credit Management a Scam?

Midland Credit Management is NOT a scam. They are a legitimate, federally regulated debt collection company subject to the Fair Debt Collection Practices Act.

However their long history includes serious legal run-ins that every consumer should know about before engaging with them.

Midland Credit Management and its parent company Encore Capital Group have faced significant regulatory action including:

A 2015 CFPB enforcement action that resulted in Encore Capital Group paying over $42 million in refunds and penalties, one of the largest debt collection enforcement actions in US history, for collecting debts consumers did not owe, filing lawsuits using false or misleading affidavits, and pressuring consumers through deceptive means.

Multiple state attorney general investigations across the country for aggressive and sometimes unlawful collection practices.

Thousands of consumer complaints filed with the Consumer Financial Protection Bureau (CFPB) for issues including collecting time barred debts, reporting inaccurate information to credit bureaus and failing to respond properly to debt validation requests.

This does not mean every interaction with Midland Credit Management is illegal or fraudulent. But it does mean you need to know your rights, verify every claim they make, and respond strategically rather than emotionally.

Who Does Midland Credit Management Collect For?

Midland Credit Management purchases charged off consumer debts from a wide range of original creditors including:

Major Credit Card Issuers: Capital One, Citibank, Synchrony Bank, Barclays and other large card issuers regularly sell their written-off balances to Midland.

Banks and Financial Institution: Large national and regional banks that have given up trying to collect past-due accounts.

Retail Store Cards: Store credit cards and retail financing accounts that went into default.

Auto Loan Deficiency Balances: The remaining balance owed after a vehicle has been repossessed and sold for less than the loan amount.

Personal Loan Lenders: Unsecured personal loan balances that were written off as uncollectable.

Medical Providers: Some medical debt portfolios are purchased through Midland affiliated companies.

Telecommunications Companies: Old phone bills, cable and internet accounts that went unpaid.

If you had a credit card with Capital One, Citibank or a major retail store and fell behind on payments several years ago, there is a very strong chance that Midland Credit Management now owns that debt.

How Did Midland Credit Management Get My Debt?

Many people are genuinely shocked when Midland Credit Management contacts them about an account they had nearly forgotten about. Here is the exact process that brought them to your door:

Step 1 | You Missed Payments on the Original Account

Whether it was a credit card, personal loan or store card, after several missed payments the original lender began the process of writing the debt off.

Step 2 | The Original Creditor Charged Off the Account

After 120 to 180 days of non-payment the original lender declared your account a “charge off”, writing it off as a business loss. A charge off appears as a severe negative mark on your credit report. The original lender may have also reported it to the credit bureaus at this point.

Step 3 | The Debt Was Sold to Midland Credit Management

The original lender sold your debt, along with thousands of other accounts, to Midland Credit Management as part of a large portfolio. The purchase price was typically between one and ten cents per dollar of face value. A $5,000 debt may have sold for as little as $50 to $500.

Step 4 | Midland Credit Management Became the New Owner

From this point forward Midland Credit Management legally owns your debt. The original lender has been paid and is no longer involved.

Step 5 | Collection Activity Begins

Midland Credit Management now attempts to collect the full original balance from you. They may send letters, make phone calls, report the debt to credit bureaus under their name, or in some cases file a lawsuit against you in court.

Understanding this process is important because it means Midland paid a tiny fraction of what they are asking you to pay, which gives you significant negotiating power that most consumers do not realize they have.

Should I Pay Midland Credit Management?

This is the most critical question, and the honest answer is: it depends entirely on your specific situation.

Paying Midland Credit Management without first doing these steps could be a very costly mistake. Go through every step before reaching for your wallet.

Step 1 | Request Written Debt Validation First

Under the Fair Debt Collection Practices Act (FDCPA) you have the absolute legal right to request written verification of any debt within 30 days of their first contact.

Send a debt validation letter via certified mail with return receipt to Midland Credit Management demanding:

- The name of the original creditor

- The original account number

- The exact total amount claimed including all interest and fees

- Complete proof that Midland Credit Management legally purchased and owns this specific debt

- The date of your last payment on the original account

Midland Credit Management must stop all collection activity while they investigate your request. If they cannot validate the debt within the required timeframe they must stop collection entirely.

Many consumers are shocked to discover that even a company as large as Midland sometimes cannot produce complete original documentation — especially for very old debts that have changed hands multiple times.

Step 2 | Verify the Statute of Limitations in Your State

Every state has a statute of limitations, a legal deadline after which a creditor can no longer successfully sue you in court to collect a debt.

This window is typically 3 to 6 years from the date of your last payment on the original account depending on your state and the type of debt.

If your debt is past the statute of limitations it is considered “time-barred.” Midland Credit Management can still contact you and ask for payment, but they cannot win a lawsuit against you for it.

This is critically important: Making even a single small payment on a time-barred debt can restart the statute of limitations clock in many states, giving Midland the legal right to sue you all over again as if the debt were fresh.

Never make any payment before confirming whether your debt is within or outside the statute of limitations.

Step 3 | Pull Your Credit Report and Verify Everything

Pull your completely free credit report from annualcreditreport.com, the only federally authorized free credit report site.

Find the Midland Credit Management entry and check:

The original creditor name and account number, does it match any account you actually had? Errors are more common than most people realize.

The date of first delinquency on the original account, this is the date that determines both the statute of limitations and the 7-year credit reporting window.

The balance claimed, does it match what you believe you owed including any added interest or fees?

Any duplicate entries, sometimes both the original creditor AND the debt buyer report the same account which is inaccurate and must be disputed.

Step 4 | Understand the 7-Year Credit Reporting Rule

Collection accounts can only legally appear on your credit report for 7 years from the date of first delinquency on the original account.

If the Midland Credit Management entry on your credit report is approaching or past the 7-year mark, paying them will NOT improve your credit score. The negative entry will fall off your report automatically on its own schedule.

Paying in this situation would simply put money in Midland’s pocket with zero benefit to you.

Step 5 | Consider Your Settlement Options

Because Midland Credit Management purchased your debt for a fraction of its face value they have enormous financial room to accept a settlement for far less than the full balance.

Most consumers who negotiate with Midland successfully settle for:

- 20 to 40 cents on the dollar on older debts

- 40 to 60 cents on the dollar on more recent debts

- Sometimes even less depending on how old the debt is and how many times it has changed hands

Never accept their first offer. Their opening number is always significantly higher than what they will actually accept.

Most importantly always negotiate a Pay for Delete agreement before paying anything. Pay for Delete means Midland Credit Management agrees in writing to completely remove the collection entry from your credit report in exchange for your payment. Always, without exception, get this agreement signed and in writing before sending a single dollar.

Midland Credit Management Lawsuit | What to Do if They Sue You

A Midland Credit Management lawsuit is one of the most stressful things a consumer can face. But understanding your options removes most of the fear.

Midland Credit Management is one of the most litigious debt buyers in America. They file thousands of lawsuits against consumers every year, and they were still actively filing new cases as recently as April 2026.

If you have received court papers from Midland Credit Management here is exactly what to do:

Do NOT Ignore the Lawsuit

This is the single most important thing to understand. Ignoring a lawsuit from Midland Credit Management results in a default judgment being entered against you, meaning they automatically win without you saying a word in your defense.

With a judgment against you Midland Credit Management can:

Garnish your wages, taking money directly from your paycheck before you even receive it.

Levy your bank account, seizing funds directly from your checking or savings account.

Place a lien on your property, which can prevent you from selling or refinancing real estate.

Respond to the Lawsuit Within the Deadline

You typically have 20 to 30 days to respond to a lawsuit depending on which state you live in. This deadline is printed on the court papers. Do not miss it.

H3: Check Whether Midland Has Proper Documentation

Midland Credit Management has a well-documented history of filing lawsuits without being able to produce complete chain of title documents proving they legally own the specific debt they are trying to collect.

When consumers respond and challenge their documentation many cases are dismissed entirely or settled for far less than the full amount, because Midland cannot prove in court that they are the legal owner of the debt.

H3: Consider a Consumer Rights Attorney

Many attorneys who specialize in FDCPA and debt collection defense cases work on contingency, meaning their fees are paid by Midland Credit Management if they win, not by you.

Getting professional legal help for a Midland Credit Management lawsuit can literally cost you nothing while potentially saving you the entire balance they claim you owe.

Negotiate a Settlement Before the Court Date

Even after being sued you can still negotiate a settlement directly with Midland Credit Management before your court date. Many debt buyers strongly prefer to settle rather than go through a full court process.

Midland Credit Management Reviews | What Real Consumers Are Saying

Midland Credit Management reviews from real consumers across multiple platforms paint a consistent picture.

The Consumer Financial Protection Bureau complaint database lists Midland Credit Management as one of the most complained-about debt collectors in the country with tens of thousands of complaints filed over the years.

The most common themes in consumer complaints include:

Attempting to Collect Debts Not Owed, Many consumers report Midland attempting to collect accounts that do not belong to them due to identity theft, mistaken identity or errors in the debt purchase process.

Reporting Inaccurate Information to Credit Bureaus, A significant number of complaints involve incorrect balances, wrong dates or duplicate entries appearing on Experian, Equifax and TransUnion reports.

Collecting Time-Barred Debts, Consumers frequently report Midland attempting to collect debts that are legally past the statute of limitations in their state.

Failing to Validate Debts Properly, Many complaints involve Midland failing to provide complete documentation when consumers exercise their right to request debt validation.

Aggressive Collection Tactics, Multiple daily calls and contact after cease and desist requests have been filed.

Midland Credit Management scams is a common search term precisely because so many consumers cannot believe that a real company is behaving the way Midland sometimes does. To be clear, Midland is a real, legitimate company. But their aggressive tactics and past legal violations explain why so many consumers question whether they are operating legitimately.

What Is the Midland Credit Management Phone Number?

The official Midland Credit Management phone number contact details are:

Customer Service: 1-800-825-8131

Midland Credit Management Address: Midland Credit Management Inc 8875 Aero Drive, Suite 200 San Diego, CA 92123

Before You Call Midland Credit Management | Know These Rules:

Never admit the debt is yours during any phone call, verbal admissions can be used against you.

Never provide your bank account or debit card information over the phone, always pay by money order or certified check if a settlement is agreed.

Always get the full name and employee ID of anyone you speak with at Midland and write down the date, time and everything discussed.

Never make a payment during a phone call, always request everything in writing first.

If they call you at work or at times prohibited by the FDCPA, before 8am or after 9pm, document it. These are violations you can take legal action on.

Your Legal Rights When Dealing With Midland Credit Management

The Fair Debt Collection Practices Act (FDCPA) gives every American powerful legal rights when dealing with Midland Credit Management or any other debt collector.

Right to Debt Validation

You can demand written proof of the debt and proof that Midland legally owns it. They must stop all collection activity while they investigate your request.

Right to Dispute Inaccurate Information

If anything Midland Credit Management reports to your credit report is wrong, wrong balance, wrong date, wrong account, you can dispute it directly with all three credit bureaus. They must investigate within 30 days.

Right to Stop All Contact

Send a written cease and desist letter by certified mail. After receiving it Midland Credit Management must stop all contact, they can only reach out to confirm the cessation or notify you of specific legal action.

Right to Sue for FDCPA Violations

If Midland Credit Management violates the FDCPA you can sue them in federal court for up to $1,000 in statutory damages plus actual damages and legal fees. Since attorneys typically handle these cases on contingency it can cost you nothing.

Right to File Official Complaints

File complaints against Midland Credit Management with:

The Consumer Financial Protection Bureau at consumerfinance.gov/complaint

The Federal Trade Commission at reportfraud.ftc.gov

Your State Attorney General’s office, find yours through naag.org

How to Remove Midland Credit Management From Your Credit Report

Getting Midland Credit Management off your credit report is one of the most impactful things you can do to improve your credit score quickly. Here are all your options:

Option 1 | Wait for Automatic Removal

Collection accounts fall off your credit report automatically after 7 years from the date of first delinquency. If the Midland entry is close to this date simply waiting may be your best strategy.

Option 2 | Dispute Inaccurate Information

If any detail reported by Midland is wrong — wrong balance, wrong date, wrong account number — file a dispute with Experian, Equifax and TransUnion. They must investigate and remove anything they cannot verify.

Option 3 | Negotiate Pay for Delete

Before making any payment negotiate a Pay for Delete agreement in writing. This means Midland agrees to remove the entry from your credit report completely in exchange for payment. Always get this signed and confirmed before sending money.

Option 4 | Challenge Debt Validation

If Midland cannot properly validate the debt within the legal timeframe you can demand they instruct credit bureaus to remove the entry. Follow up with written documentation of their failure to validate.

Step by Step Action Plan | What to Do Right Now

Here is your complete roadmap for dealing with Midland Credit Management:

Step 1 | Stay Calm and Think Strategically

Millions of Americans deal with Midland Credit Management every year. This is manageable. Panic leads to mistakes. Knowledge leads to solutions.

Step 2 | Do Not Pay Anything Yet

Making a premature payment can restart the statute of limitations, waive important legal rights and cost you money that may not even help your credit score. Wait until you have completed every step below.

Step 3 | Pull Your Free Credit Report

Go to annualcreditreport.com right now. Pull all three reports, Experian, Equifax and TransUnion. Find the Midland Credit Management entry and document everything.

Step 4 | Check the Statute of Limitations

Find the date of your last payment on the original account. Look up your specific state’s statute of limitations on debt collection. Confirm whether Midland can legally sue you or not.

Step 5 | Send a Debt Validation Letter

If it has been less than 30 days since Midland first contacted you send a written debt validation request via certified mail with return receipt immediately.

Step 6 | Choose Your Strategy

| Your Situation | Recommended Strategy |

|---|---|

| Debt is time-barred | Send cease and desist, do not pay |

| Debt is valid and recent | Negotiate settlement with pay for delete |

| Debt is not yours | Dispute with credit bureaus immediately |

| Lawsuit received | Contact consumer attorney immediately |

| Close to 7-year mark | Wait for automatic removal |

| Want fast credit repair | Negotiate pay for delete before paying |

Step 7 | Get Absolutely Everything in Writing

Whatever agreement you reach with Midland Credit Management, get it in writing with signatures before sending any payment. Verbal promises from debt collectors are worth nothing and are extremely difficult to enforce.

Step 8 | Follow Up After Resolution

After any payment or dispute resolution, check your credit report again within 30 to 60 days to confirm that Midland has updated the entry correctly. If they have not, dispute immediately.

If you are dealing with overwhelming debt beyond just this one collection account, exploring your complete options is essential. Check out our get out of debt category for comprehensive guides on debt payoff strategies, budgeting and financial recovery.

Frequently Asked Questions About Midland Credit Management

What is Midland Credit Management?

Midland Credit Management is a debt buying company and subsidiary of Encore Capital Group. They purchase portfolios of charged off consumer debts from banks and credit card companies for pennies on the dollar and then attempt to collect the full balance from consumers.

Is Midland Credit Management legit?

es. Midland Credit Management is a legitimate, registered debt collection company subject to federal law. However they have faced significant regulatory action and have thousands of consumer complaints on file. Always know your rights when dealing with them.

Should I pay Midland Credit Management?

Not without doing your homework first. Check the statute of limitations, validate the debt, verify your credit report and understand the 7-year reporting window before making any decision. If you do decide to pay, always negotiate a Pay for Delete agreement in writing first.

Can Midland Credit Management sue me?

Yes, if the debt is within your state’s statute of limitations Midland Credit Management can and does file lawsuits. They are one of the most active litigating debt buyers in the country. Never ignore court papers. Always respond within the deadline.

What is the Midland Credit Management phone number?

The official customer service number is 1-800-825-8131. Before calling know exactly what you want to say, never admit the debt is yours and never provide banking information over the phone.

How do I remove Midland Credit Management from my credit report?

Your options are to wait for the 7 year automatic removal, dispute any inaccurate information with the credit bureaus, negotiate a Pay for Delete settlement, or challenge their debt validation. The fastest method with the most benefit to your credit score is negotiating a Pay for Delete agreement before making any payment.

Are Midland Credit Management scams real?

Midland Credit Management is a legitimate company, not a scam operation. However they have a documented history of aggressive and sometimes unlawful practices. The 2015 CFPB enforcement action requiring $42 million in refunds confirms they have violated consumer rights at scale. Always verify any communication you receive and know your rights.

For more information on managing your finances beyond debt collection, our 50/30/20 budget rule guide is a great starting point for building a sustainable financial plan.

The Bottom Line on Midland Credit Management

Midland Credit Management is one of the largest, most aggressive debt buyers in America. They are legitimate, but they have a well-documented history of pushing boundaries and a track record of regulatory penalties that every consumer should know about.

The bottom line is simple: you have significantly more power in this situation than they want you to believe.

Before you pay a single dollar:

Pull your credit report and verify everything they claim.

Check your state’s statute of limitations.

Request written debt validation.

Understand exactly where you are in the 7-year credit reporting window.

Negotiate, never pay full balance and always demand Pay for Delete in writing.

Should you pay Midland Credit Management? Sometimes yes, when the debt is valid, properly documented and when paying genuinely moves your financial situation forward. But never pay out of fear or without understanding every option available to you first.

The Americans who come out best when dealing with Midland Credit Management are the ones who stay calm, know the law and respond strategically. That is exactly what this guide equips you to do.

Start your path to financial freedom today, browse all our save money and debt management guides to build a complete financial recovery plan that goes far beyond handling one debt collector.