Managing money can feel overwhelming when you don’t have a clear system. That’s why the 50/30/20 budget rule has become one of the most popular personal finance methods in the United States.

It is simple, flexible, and designed to help you control spending, build savings, and reduce financial stress without complicated tools or spreadsheets.

In this guide, you’ll learn exactly how the 50/30/20 rule works, real life examples, and how to apply it to your monthly income.

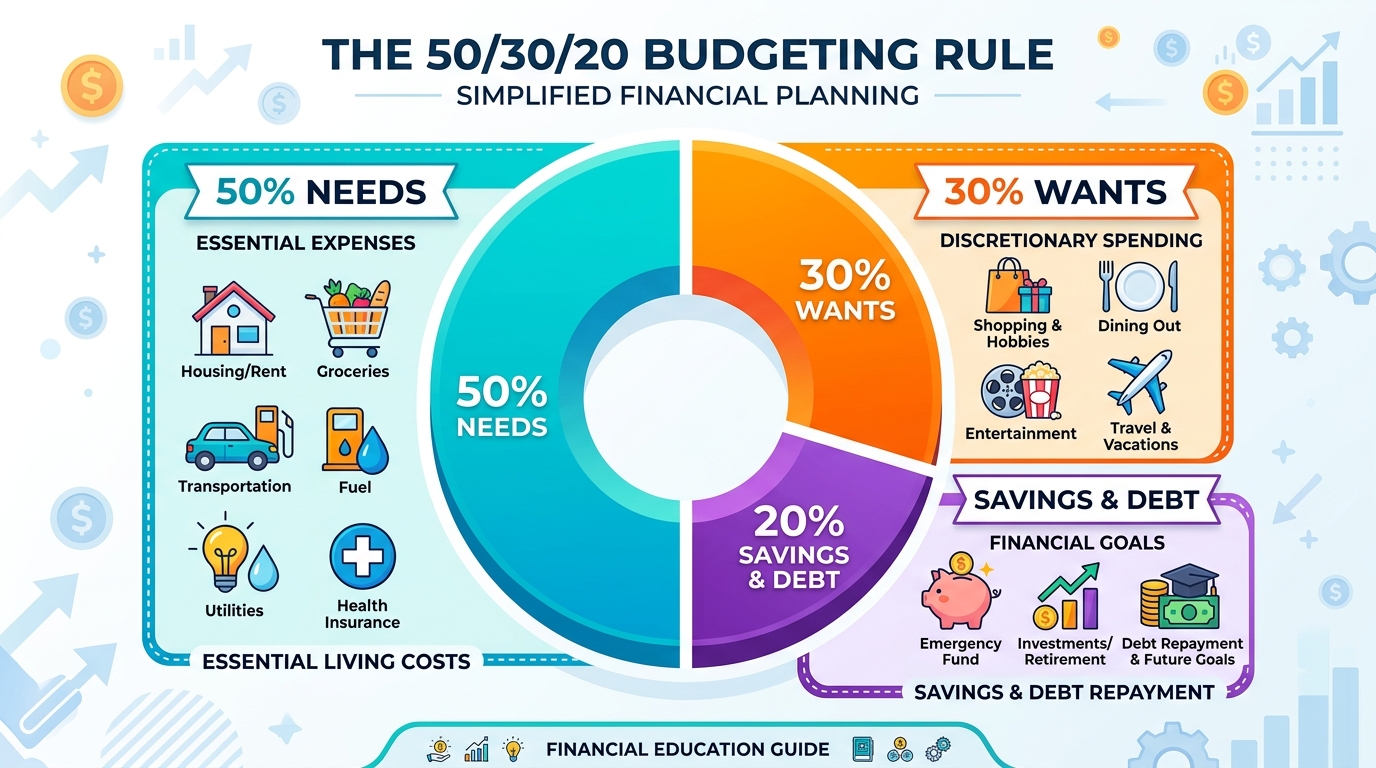

What Is the 50/30/20 Budget Rule?

The 50/30/20 budget rule is a personal finance framework where you divide your after-tax income into three spending categories:

- 50% for needs

- 30% for wants

- 20% for savings and debt repayment

This method helps you create a balanced budget that covers essentials while still allowing room for lifestyle spending and long term financial goals.

According to the Consumer Financial Protection Bureau, creating a simple budget helps consumers track spending and improve financial stability over time.

50/30/20 Budget Rule Breakdown (Simple Table)

| Category | Percentage | Meaning | Examples |

|---|---|---|---|

| Needs | 50% | Essential living expenses | Rent, groceries, utilities, transportation |

| Wants | 30% | Lifestyle and non-essential spending | Dining out, shopping, subscriptions, entertainment |

| Savings & Debt | 20% | Financial growth and debt reduction | Emergency fund, investments, credit card payments |

How the 50/30/20 Budget Rule Works (Real Example)

Let’s say your monthly after tax income is $3,000.

50% Needs = $1,500

This portion covers your essential living expenses such as:

- Rent or housing payments

- Utility bills (electricity, water, internet)

- Groceries and food

- Transportation costs

👉 These are non negotiable expenses required for daily living.

30% Wants = $900

This category includes lifestyle and discretionary spending:

- Dining out and takeaways

- Streaming services and subscriptions

- Shopping and personal items

- Entertainment and hobbies

👉 These are flexible expenses that improve your lifestyle but are not essential.

20% Savings & Debt = $600

This portion is used for financial stability and future goals:

- Emergency savings fund

- Retirement or investments

- Credit card or loan repayments

- Building financial security

👉 This is the most important part for long term financial health.

Why the 50/30/20 Budget Rule Is So Popular

The 50/30/20 budgeting method is widely used because it is:

- Easy to understand for beginners

- Flexible for different income levels

- Effective for controlling overspending

- Helpful for building savings habits

- Simple enough to follow without financial tools

Unlike complex budgeting systems, this rule focuses on clarity and consistency rather than strict tracking.

The budgeting method is widely explained by Investopedia as a simple framework for managing personal income effectively.

Who Should Use the 50/30/20 Budget Rule?

This budgeting method is ideal for:

- Beginners learning personal finance

- Students managing limited income

- Individuals living paycheck to paycheck

- People trying to reduce debt

- Anyone looking for a simple budgeting system

If you struggle with overspending or lack of savings, this method can help bring structure to your finances.

Common Mistakes to Avoid

Even though this method is simple, many people misuse it.

1. Misclassifying Expenses

Sometimes people treat luxury spending as “needs,” which breaks the balance of the budget.

2. Ignoring Debt Repayment

The 20% savings category should also include debt repayment strategy, especially for credit cards and personal loans.

3. Not Adjusting for Real Life

In expensive cities, rent may exceed 50%. The rule should be adapted, not followed blindly.

50/30/20 Budget Rule vs Other Budgeting Methods

| Method | Complexity | Best For |

|---|---|---|

| 50/30/20 Rule | Easy | Beginners and simple budgeting |

| Zero-Based Budgeting | Advanced | Detailed financial control |

| Envelope System | Medium | Cash based spending control |

The 50/30/20 method is often the best starting point before moving to advanced budgeting systems.

How to Start Using the 50/30/20 Budget Rule

Follow these simple steps: build a monthly budget plan

- Calculate your monthly after-tax income

- Divide it into 50%, 30%, and 20%

- Assign expenses to each category

- Track spending for one month

- Adjust based on your lifestyle

Consistency is more important than perfection.

Final Thoughts

The 50/30/20 budget rule is one of the simplest and most effective money management strategies for beginners.

It helps you:

- Control expenses

- Build savings habits and get out of debt faster

- Reduce financial stress

- Stay financially organized

- Side hustles to increase income

If you are just starting your personal finance journey, this method is a strong foundation for long-term financial stability.

FAQs About 50/30/20 Budget Rule

What is the 50/30/20 budget rule?

It is a budgeting method that divides income into 50% needs, 30% wants, and 20% savings or debt repayment

It is a budgeting method that divides income into 50% needs, 30% wants, and 20% savings or debt repayment.

Yes, it is one of the easiest budgeting systems for people new to personal finance.

Can I modify the 50/30/20 rule?

Yes, you can adjust the percentages based on your income and expenses. For example if rent is high in your city you may need 60% for needs and reduce wants to 20%

Does the 20% include debt repayment?

Yes, savings and debt repayment are both included in the 20% category.