LVNV Funding LLC: What Is It, Is It Legit and Should You Pay?

If LVNV Funding LLC has shown up on your credit report or contacted you about an old debt, you are probably feeling confused, stressed and unsure what your next move should be. Similar to the unifin debt collector you should act fast.

Who exactly is LVNV Funding LLC? Are they legitimate? Do you actually owe them money? And most importantly, should you pay them?

These are exactly the right questions to be asking. Because paying a debt collector without understanding your rights first can be a very costly mistake.

In this complete guide you will learn everything you need to know about LVNV Funding LLC, what they are, who they collect for, what your legal rights are, and the exact steps to take right now to protect yourself.

What Is LVNV Funding LLC?

LVNV Funding LLC is a debt collection company, specifically a debt buyer, based in Greenville, South Carolina. They purchase old, unpaid debts from original creditors like banks, credit card companies, and other lenders for a fraction of what those debts are worth.

Once LVNV Funding LLC purchases your debt, they become the new legal owner of it. They then attempt to collect the full original balance from you, even though they paid far less than that to acquire it.

LVNV Funding LLC is owned by Resurgent Capital Services, which is itself owned by Sherman Financial Group, one of the largest debt buying companies in the United States.

So to answer the first question directly: LVNV Funding LLC is a real, legitimate company. They are not a scam. However legitimate does not mean you are automatically required to pay them, and it certainly does not mean you should pay without doing your research first.

LVNV Funding LLC operates similarly to other large debt buyers like Portfolio Recovery Associates, they purchase your old debt for pennies on the dollar and then attempt to collect the full balance from you. Understanding how this process works gives you a significant advantage when dealing with them.

Who Does LVNV Funding LLC Collect For?

Understanding who does LVNV Funding LLC collect for helps you figure out where your debt originally came from.

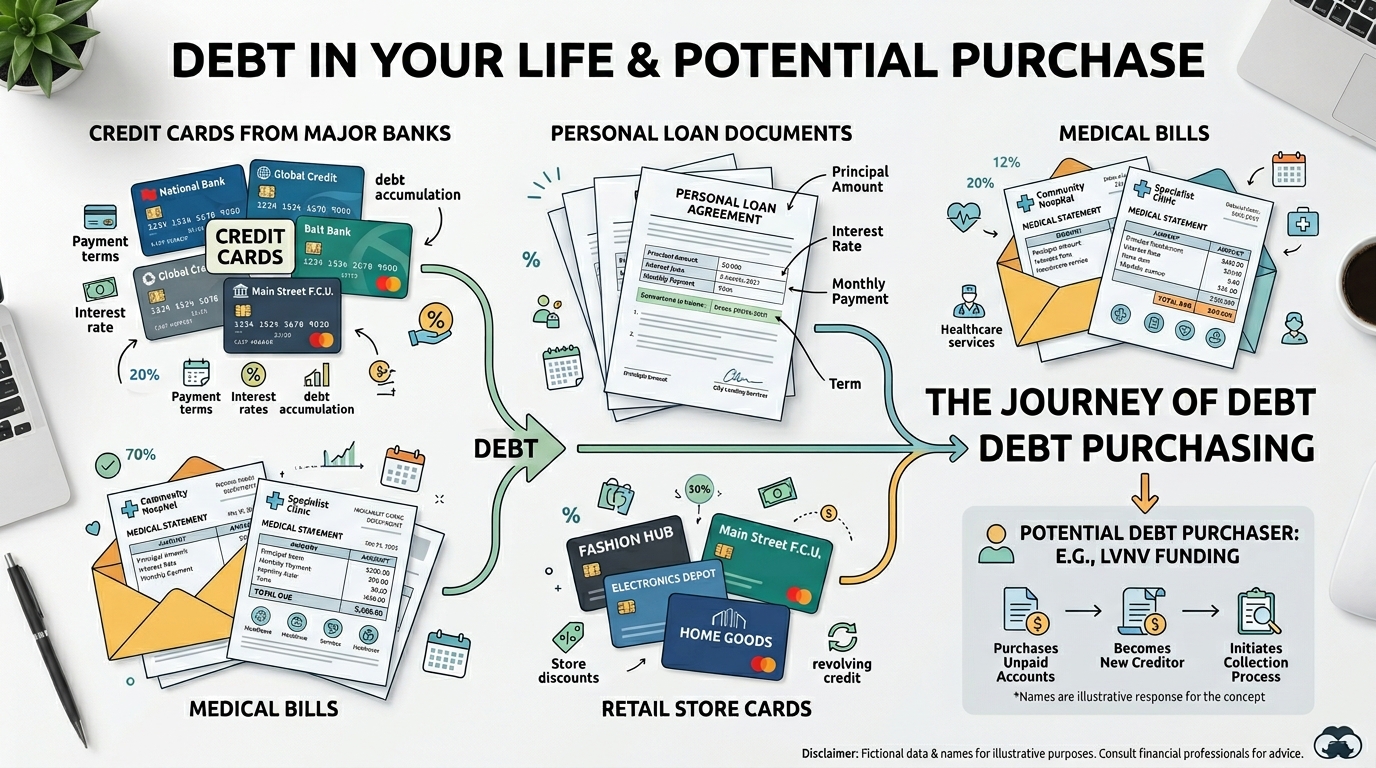

LVNV Funding LLC typically purchases debts that originated from:

Credit Card Companies, They frequently buy charged-off credit card balances from major issuers including Credit One Bank, Citibank, Capital One, and Synchrony Bank.

Personal Loan Lenders, Unpaid personal loans from online lenders and banks often end up with LVNV Funding after they are written off.

Retail Store Cards, Store credit cards and retail financing accounts that went into default.

Auto Loans, Deficiency balances from repossessed vehicles.

Medical Debt, Unpaid medical bills purchased from hospitals and healthcare providers.

Telecommunications Debt, Old phone bills and cable account balances.

If you had an account with Credit One Bank in particular, there is a very strong chance that LVNV Funding LLC credit one bank accounts make up a large portion of their collection portfolio. Many consumers who had Credit One Bank credit cards and fell behind on payments find LVNV Funding on their credit report years later.

Is LVNV Funding LLC Legit or a Scam?

LVNV Funding LLC is a legitimate, registered debt collection company. They are licensed to operate in most states and are subject to federal debt collection laws.

However that does not mean they always operate cleanly.

LVNV Funding LLC has one of the highest complaint volumes of any debt buyer in the United States. The Consumer Financial Protection Bureau (CFPB) has received thousands of consumer complaints against them involving:

Attempting to collect debts past the statute of limitations, Trying to collect on debts that are legally too old to be enforced in court.

Reporting inaccurate information to credit bureaus, Listing incorrect balances, wrong dates, or accounts that do not belong to the consumer.

Failing to verify debts when requested, Not responding properly to debt validation requests as required by law.

Filing lawsuits without proper documentation, Taking consumers to court without being able to prove the debt is valid or that they legally own it.

Contacting consumers excessively, Calling multiple times per day in violation of the Fair Debt Collection Practices Act.

This track record of complaints means you need to be careful and strategic when dealing with LVNV Funding LLC, not panicked and reactive.

How Did LVNV Funding LLC Get My Debt?

Many people are shocked when LVNV Funding LLC contacts them about an old account they had forgotten about. Here is exactly how that happens:

Step 1 — Your Original Account Goes Delinquent

You miss payments on a credit card, personal loan, or other account. The original creditor tries to collect for several months, usually 90 to 180 days.

Step 2 — The Original Creditor Charges Off the Debt

After enough missed payments the original lender writes the debt off as a loss on their books. This is called a “charge off.” The charge off appears on your credit report as a negative mark.

Step 3 — The Debt Is Sold to LVNV Funding LLC

The original creditor sells the charged-off debt to LVNV Funding LLC for typically one to ten cents per dollar owed. So if you owed $3,000 they may have paid just $30 to $300 for your debt.

Step 4 — LVNV Funding LLC Begins Collection

Now that they legally own your debt LVNV Funding LLC begins attempting to collect the full original balance from you, despite having paid a tiny fraction of it.

Step 5 — They Contact You

You start receiving letters, phone calls, and eventually your debt may appear on your credit report under the LVNV Funding LLC name.

This entire process is completely legal. But it also means they have enormous room to negotiate since they paid so little for your debt.

Should I Pay LVNV Funding LLC?

This is the most important question, and the honest answer is: it depends entirely on your specific situation.

Never make a payment to LVNV Funding LLC without first going through these critical steps:

Step 1 — Request Debt Validation Immediately

Under the Fair Debt Collection Practices Act (FDCPA) you have the legal right to demand written verification of any debt within 30 days of their first contact.

Send a written debt validation letter via certified mail with return receipt requesting:

- The name of the original creditor

- The original account number

- The exact amount owed including interest and fees

- Proof that LVNV Funding LLC legally owns the debt

If they cannot validate the debt they must stop all collection activity immediately. Many consumers are shocked to discover that debt buyers sometimes cannot produce proper documentation, especially for older debts that have changed hands multiple times.

Step 2 — Check the Statute of Limitations

Every state has a legal time limit, called the statute of limitations, after which a creditor can no longer sue you in court to collect a debt.

This ranges from 3 to 6 years in most states depending on the type of debt.

Why this is critical: If your debt is past the statute of limitations it is considered “time-barred.” LVNV Funding LLC can still ask you to pay, but they cannot successfully sue you for it.

Extreme warning: Making even a small partial payment on a time-barred debt can restart the statute of limitations in some states, giving them the legal right to sue you all over again. Never make any payment before confirming whether the debt is time-barred.

Step 3 — Check Your Credit Report

Pull your free credit report from annualcreditreport.com and find the LVNV Funding LLC entry.

Verify:

- The original account name and number match your records

- The balance they claim is accurate

- The date of first delinquency, this determines both the statute of limitations and the 7-year credit reporting window

- Whether any information appears inaccurate or incorrect

If anything is wrong you have the right to dispute it directly with the credit bureaus.

Step 4 — Understand the Credit Reporting Timeline

Collection accounts can only legally appear on your credit report for 7 years from the date of first delinquency on the original account.

Paying a collection account that is close to the 7-year mark will NOT improve your credit score, the negative entry will fall off your report on its own very soon.

Paying simply puts money in LVNV Funding LLC’s pocket without helping your credit at all. Understanding this timeline is crucial before making any financial decision.

Step 5 — Consider Negotiating a Settlement

Because LVNV Funding LLC purchased your debt for pennies on the dollar they have enormous room to accept far less than the full balance.

Most consumers successfully negotiate settlements for:

- 20 to 40 cents on the dollar for older debts

- 40 to 60 cents on the dollar for newer debts

Never accept their first offer. Their opening number is always higher than what they will actually accept.

Most importantly: Always negotiate a Pay for Delete agreement. This means they agree in writing to completely remove the LVNV Funding LLC entry from your credit report in exchange for your payment. Always get this agreement in writing and signed before sending a single dollar.

What Is the LVNV Funding LLC Phone Number?

If you need to contact LVNV Funding LLC directly here is their official contact information:

LVNV Funding LLC Phone Number: 1-800-363-3492

LVNV Funding LLC Address: LVNV Funding LLC c/o Resurgent Capital Services PO Box 10587 Greenville, SC 29603

LVNV Funding LLC Greenville Office: 55 Beattie Place, Suite 110 Greenville, SC 29601

Before calling them:

- Know exactly what you want to say

- Decide whether you are calling to dispute, validate, negotiate or cease contact

- Never admit the debt is yours over the phone

- Never give banking information over the phone

- Write down everything said including the date, time and name of the representative

LVNV Funding LLC Reviews | What Are Consumers Saying?

LVNV Funding LLC reviews from real consumers paint a consistent picture across multiple complaint platforms.

On the Consumer Financial Protection Bureau (CFPB) complaint database LVNV Funding LLC has received over 10,000 complaints, making them one of the most complained-about debt collectors in the United States.

Common themes in consumer complaints include:

Debt Not Theirs | Many consumers report LVNV Funding attempting to collect debts that do not belong to them, either due to identity theft, mistaken identity, or errors in the debt purchasing process.

Unable to Verify the Debt | A significant number of complaints involve LVNV Funding failing to provide proper documentation when consumers request debt validation.

Credit Report Errors | Consumers frequently report inaccurate information being reported to Equifax, Experian and TransUnion, including wrong balances, wrong dates and duplicate entries.

Collecting on Time-Barred Debts | Numerous complaints involve LVNV Funding attempting to collect debts that are past the legal statute of limitations in the consumer’s state.

Aggressive Communication | Multiple daily calls and contact attempts despite cease and desist requests.

This pattern of complaints is why knowing your rights before responding to LVNV Funding LLC is absolutely essential.

Has LVNV Funding LLC Filed a Lawsuit Against You?

An LVNV Funding LLC lawsuit requires immediate action. Do not ignore court papers under any circumstances.

Ignoring a lawsuit from LVNV Funding LLC results in a default judgment against you, meaning they automatically win without you presenting any defense whatsoever.

What to Do If You Receive an LVNV Funding LLC Lawsuit

Act immediately, you typically have only 20 to 30 days to respond depending on your state.

Check the documentation carefully: LVNV Funding LLC has a documented history of filing lawsuits without being able to produce proper chain of title documents proving they legally own the debt. Many lawsuits are dismissed when consumers respond and challenge their documentation.

Consider hiring a consumer rights attorney: Many attorneys who specialize in FDCPA cases work on contingency, meaning they get paid by LVNV Funding if they win, not by you. Getting legal help can literally cost you nothing.

Raise the statute of limitations defense: If the debt is time-barred this is a powerful legal defense that can get the case dismissed entirely.

Negotiate a settlement before the court date: Even after being sued you can negotiate a settlement. Many debt buyers prefer to settle rather than go through a full court process.

Your Legal Rights When Dealing With LVNV Funding LLC

The Fair Debt Collection Practices Act (FDCPA) gives you powerful rights that LVNV Funding LLC must respect:

Right to Debt Validation

You can demand written proof that the debt is valid and that LVNV Funding LLC has the legal right to collect it. They must stop all collection activity while they investigate.

Right to Dispute Inaccurate Information

If anything on your credit report related to LVNV Funding is wrong you can dispute it directly with the credit bureaus, Experian, Equifax and TransUnion. They are legally required to investigate within 30 days.

Right to Stop All Contact

Send a written cease and desist letter via certified mail and LVNV Funding LLC must stop all contact with you. After receiving it they can only contact you to confirm they are stopping or to notify you of specific legal action.

Right to Sue for FDCPA Violations

If LVNV Funding LLC violates the FDCPA you can sue them in federal court for up to $1,000 in statutory damages plus actual damages and attorney fees, and you will likely not pay a cent because attorneys handle these cases on contingency.

Right to File Complaints

You can file complaints against LVNV Funding LLC with:

- CFPB at consumerfinance.gov/complaint

- FTC at reportfraud.ftc.gov

- Your state attorney general’s office

How to Remove LVNV Funding LLC From Your Credit Report

Removing LVNV Funding LLC from your credit report is one of the most effective ways to improve your credit score quickly. Here are your options:

Option 1 | Wait for the 7-Year Drop Off

If the account is approaching 7 years from the date of first delinquency it will fall off your credit report automatically. No action required.

Option 2 | Dispute Inaccurate Information

If any information reported by LVNV Funding LLC is inaccurate — wrong balance, wrong date, wrong account number — dispute it with all three credit bureaus. If they cannot verify the accurate information they must remove it.

Option 3 | Negotiate Pay for Delete

Offer to pay a settlement in exchange for complete removal of the LVNV Funding LLC entry from your credit report. Get the agreement in writing before paying.

Option 4 | Debt Validation Challenge

If LVNV Funding cannot properly validate the debt within the legal timeframe send a follow-up letter demanding they instruct the credit bureaus to remove the account. If they fail to respond properly you have grounds for a dispute.

Step by Step Action Plan — What to Do Right Now

Here is your complete action plan for dealing with LVNV Funding LLC:

Step 1 — Stay Calm and Do Not Panic

Millions of Americans deal with debt collectors every year. This is a manageable situation.

Step 2 — Do Not Pay Anything Yet

Wait until you have completed all the steps below. Premature payment can restart the statute of limitations and may not even help your credit.

Step 3 — Pull Your Credit Report

Go to annualcreditreport.com, free for all Americans. Find the LVNV Funding LLC entry and document all details.

Step 4 — Confirm the Statute of Limitations

Find your last payment date on the original account. Look up your state’s specific statute of limitations on debt. Confirm whether the debt is time-barred.

Step 5 — Send a Debt Validation Letter

If it has been less than 30 days since first contact send your validation letter via certified mail immediately.

Step 6 — Decide Your Strategy Based on Your Situation

| Your Situation | Best Strategy |

|---|---|

| Debt is time-barred | Send cease and desist, do not pay |

| Debt is valid and recent | Negotiate settlement with pay for delete |

| Debt is not yours | Dispute immediately with credit bureaus |

| Lawsuit received | Contact consumer attorney immediately |

| Close to 7 year mark | Wait for automatic removal |

| Want to rebuild credit fast | Negotiate pay for delete agreement |

Step 7 — Get Everything in Writing

Whatever agreement you reach get it in writing with signatures before making any payment. Verbal agreements are worthless.

Step 8 — Follow Up

After any payment confirm the credit bureaus have updated your report correctly. If not dispute the remaining entry immediately.

Dealing with debt collectors like LVNV Funding LLC is just one piece of your overall financial picture. If you are ready to take full control of your debt situation beyond just handling this one collector, browse our complete get out of debt guides where we cover debt payoff strategies, budgeting methods and everything else you need to become completely debt free.

Frequently Asked Questions About LVNV Funding LLC

What is LVNV Funding LLC?

LVNV Funding LLC is a debt buying company owned by Resurgent Capital Services and Sherman Financial Group. They purchase old charged-off debts from original creditors for pennies on the dollar and then attempt to collect the full balance from consumers.

Is LVNV Funding LLC a scam?

No. LVNV Funding LLC is a legitimate, registered debt collection company subject to federal law. However they have a significant complaint history and you should know your rights before engaging with them.

Who does LVNV Funding LLC collect for?

LVNV Funding LLC primarily collects debts originally owed to credit card companies including Credit One Bank, Citibank and Capital One, as well as personal loan lenders, retail store cards, auto loan deficiency balances and medical providers.

Can LVNV Funding LLC sue me?

Yes, if the debt is within your state’s statute of limitations LVNV Funding LLC can and does file lawsuits. However they often struggle to produce proper documentation in court. Never ignore a lawsuit, always respond.

Can I negotiate with LVNV Funding LLC?

Absolutely. Since they bought your debt for a very small fraction of its value they have significant room to settle. Most consumers successfully negotiate settlements between 20 and 50 cents on the dollar. Always get the final agreement in writing.

How do I get LVNV Funding LLC off my credit report?

Your options are to wait for the 7-year automatic removal, dispute inaccurate information with the credit bureaus, negotiate a pay for delete agreement, or challenge their debt validation. The fastest method for most consumers is negotiating a pay for delete settlement.

What if I cannot afford to pay LVNV Funding LLC?

If you genuinely cannot afford to pay contact a nonprofit credit counseling agency for free guidance. You can also send a cease and desist letter to stop their contact. If the debt is time-barred or approaching the 7-year credit reporting window you may be better off waiting rather than paying.

The Bottom Line on LVNV Funding LLC

Dealing with LVNV Funding LLC is stressful, but you have significantly more power in this situation than you probably realize.

Before paying anything:

- Pull your credit report and verify all information

- Check your state’s statute of limitations

- Request written debt validation

- Understand exactly how close the account is to the 7-year removal date

- Negotiate a settlement or pay for delete if payment makes sense

- Get every agreement in writing before sending money

Once you have dealt with LVNV Funding LLC and stabilized your debt situation the next step is keeping more money in your pocket every month. Our save money guides are packed with practical tips that everyday Americans are using right now to cut expenses and build financial security from zero.

Should you pay LVNV Funding LLC? Sometimes yes, when the debt is valid, properly documented and paying genuinely benefits your financial situation. But never pay out of fear, and never pay without understanding every option available to you first.

The most successful consumers are those who stay calm, know their rights and respond strategically rather than either ignoring the problem or paying immediately out of panic.

You have legal rights. Use them.