If Portfolio Recovery Associates (debt collector) has contacted you about an old debt, you are probably feeling stressed, confused, and unsure what to do next.

Should you pay them? Should you ignore them? Could they sue you? Is Portfolio Recovery Associates LLC even a legitimate company?

These are exactly the right questions to ask, and in this guide you will get honest, clear answers to every single one of them.

Before you make any payment or pick up the phone, read this entire article. What you learn here could save you hundreds or even thousands of dollars.

What Is Portfolio Recovery Associates?

Portfolio Recovery Associates (also known as Portfolio Recovery Associates LLC) is one of the largest debt collection companies in the United States.

They are a debt buyer, meaning they purchase old, unpaid debts from original creditors like banks, credit card companies, and medical providers for pennies on the dollar. Once they buy your debt, they become the new owner and attempt to collect the full balance from you.

Portfolio Recovery Associates LLC is headquartered in Norfolk, Virginia and has been operating since 1996. They are a subsidiary of PRA Group, a publicly traded company on the Nasdaq stock exchange.

So to answer the first question directly, yes, Portfolio Recovery Associates is a real, legitimate company. They are not a scam. However that does not mean you are automatically obligated to pay them, and it certainly does not mean you should pay without doing your research first.

Is Portfolio Recovery Associates Legit or a Scam?

Portfolio Recovery Associates is a legitimate debt collection company regulated by the Fair Debt Collection Practices Act (FDCPA).

However legitimate does not mean they always operate perfectly. Portfolio Recovery Associates has faced significant legal scrutiny over the years.

The Consumer Financial Protection Bureau (CFPB) has taken action against Portfolio Recovery Associates on multiple occasions for:

- Attempting to collect debts that were already past the legal statute of limitations

- Making false representations about debts owed

- Filing lawsuits against consumers without proper documentation

- Failing to properly investigate consumer disputes

In fact the CFPB ordered Portfolio Recovery Associates to pay over $19 million in refunds and penalties in 2015 for illegal debt collection practices.

This history is important because it means you have real legal rights when dealing with them — and those rights can protect you significantly.

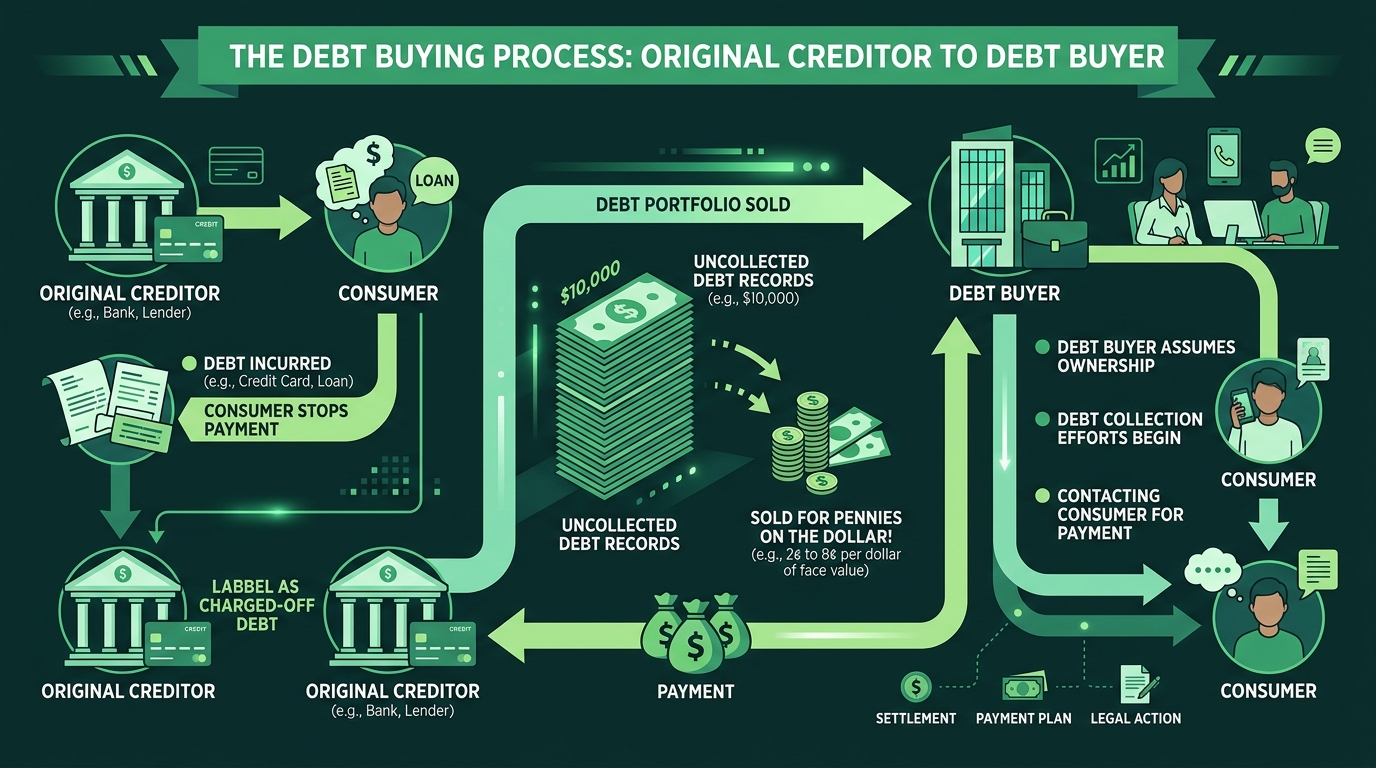

How Does Portfolio Recovery Associates Get Your Debt?

Understanding how Portfolio Recovery Associates LLC acquires debt helps you understand your situation better.

Here is how the process works:

Step 1 — Original creditor gives up collecting

Your original lender, a credit card company, bank or medical provider, decides the debt is too old or too difficult to collect themselves.

Step 2 — They sell the debt for pennies

The original creditor sells your debt to Portfolio Recovery Associates for typically 1 to 10 cents per dollar owed. So if you owe $5,000, they may have paid only $50 to $500 for it.

Step 3 — Portfolio Recovery Associates attempts collection

They now own your debt and begin attempting to collect the full amount from you, even though they paid far less than the face value.

Step 4 — They contact you

You start receiving letters, calls and potentially legal notices from Portfolio Recovery Associates.

This process is completely legal. But it also means they have significant room to negotiate because they paid so little for your debt in the first place.

Should I Pay Portfolio Recovery Associates?

This is the most important question, and the honest answer is: it depends on your specific situation.

Here are the key factors you must consider before making any payment:

Factor 1 — Check the Statute of Limitations

Every state has a statute of limitations on debt collection, a legal time limit after which creditors can no longer sue you to collect a debt.

In most states this ranges from 3 to 6 years from the date of your last payment or activity on the account.

Why this matters: If your debt is past the statute of limitations in your state it is considered “time barred.” Portfolio Recovery Associates can still ask you to pay, but they cannot legally sue you to force payment.

What to do: Find out when you last made a payment on this debt. Then look up the statute of limitations for your specific state. If the debt is time-barred you have significantly more leverage.

Critical warning: Making even a small partial payment on a time-barred debt can restart the statute of limitations in some states, giving Portfolio Recovery Associates the legal right to sue you again. Never make any payment without first confirming the debt status.

Factor 2 — Verify the Debt Is Actually Yours

Before paying anything always request a debt validation letter from Portfolio Recovery Associates.

Under the Fair Debt Collection Practices Act you have the legal right to request written verification of any debt. Portfolio Recovery Associates must provide:

- The name of the original creditor

- The original account number

- The total amount owed including interest and fees

- Proof that they legally own the debt

If they cannot verify the debt they are legally required to stop all collection activity. Many consumers are surprised to find that debt buyers sometimes cannot produce proper documentation, especially for older debts.

How to request validation: Send a written debt validation request via certified mail with return receipt within 30 days of their first contact. Keep copies of everything.

Factor 3 — Check Your Credit Report First

Pull your free credit report from annualcreditreport.com and look for the Portfolio Recovery Associates entry.

Check:

- The original account name and number

- The date the account was opened and when it went delinquent

- The balance they claim you owe

- Whether it is within the credit reporting time limit (7 years)

If the debt is older than 7 years it should not appear on your credit report at all. Paying it will NOT improve your credit score, it will simply put money in their pocket.

Factor 4 — Consider Negotiating a Settlement

Because Portfolio Recovery Associates LLC bought your debt for pennies on the dollar they have enormous room to settle for less than the full amount.

In many cases consumers successfully negotiate settlements for:

- 25 to 50 cents on the dollar for older debts

- 40 to 60 cents on the dollar for newer debts

- Sometimes even less depending on how old the debt is

Never accept their first offer. Their first offer is always higher than what they will actually accept.

Factor 5 — Understand the Impact on Your Credit

Paying Portfolio Recovery Associates affects your credit differently depending on how you pay:

| Payment Type | Credit Impact |

|---|---|

| Pay in Full | Account updates to “Paid” but collection entry remains for 7 years |

| Settle for Less | Account shows “Settled” still stays 7 years |

| Pay for Delete | Collection entry removed entirely, best option |

| Ignore It | Debt remains, possible lawsuit, wage garnishment |

Pay for Delete is the best outcome. This means negotiating an agreement where Portfolio Recovery Associates removes the collection entry from your credit report entirely in exchange for payment. Always get this agreement in writing before paying a single dollar.

What Happens If You Ignore Portfolio Recovery Associates?

Many people wonder what happens if they simply do not respond or pay.

Here is the honest answer:

If the debt is within the statute of limitations Portfolio Recovery Associates can and does file lawsuits against consumers. If they win a judgment against you they can:

- Garnish your wages

- Levy your bank account

- Place liens on your property

Ignoring them when the debt is collectible is one of the worst things you can do.

If the debt is past the statute of limitations ignoring them carries less immediate legal risk, but they may still continue calling and the debt may still affect your credit score.

Either way ignoring the situation completely is rarely the right strategy. Understanding your rights and responding strategically is always better.

What Is the Portfolio Recovery Associates Phone Number?

The official Portfolio Recovery Associates phone number is:

1-800-772-1413

Their mailing address is: Portfolio Recovery Associates LLC 120 Corporate Boulevard Norfolk, VA 23502

Important: Before calling them understand what you want to say. Know whether you want to:

- Request debt validation

- Negotiate a settlement

- Dispute the debt

- Request they stop contacting you

Going into the call without a plan puts you at a disadvantage. Consider writing down your key points before calling.

Has Portfolio Recovery Associates Filed a Lawsuit Against You?

A Portfolio Recovery Associates lawsuit is a serious matter that requires immediate action.

If you have received court papers from Portfolio Recovery Associates do not ignore them. Ignoring a lawsuit results in a default judgment against you, meaning they automatically win without you even making your case.

What to do if you receive a Portfolio Recovery Associates lawsuit:

Step 1 — Read the documents carefully

Note the response deadline — usually 20 to 30 days depending on your state.

Step 2 — Consider your options

- Respond yourself (called a pro se defense)

- Hire a consumer rights attorney

- Negotiate a settlement before the court date

Step 3 — Check for FDCPA violations

Many Portfolio Recovery Associates lawsuits are dismissed or settled because they cannot produce proper documentation of the original debt. A consumer rights attorney can identify these weaknesses.

Step 4 — Know that help is free

Consumer rights attorneys who handle FDCPA cases often work on contingency, meaning they get paid by Portfolio Recovery Associates if they win, not by you. Getting legal help for debt collection lawsuits can literally cost you nothing.

Your Legal Rights When Dealing With Portfolio Recovery Associates

Under the Fair Debt Collection Practices Act (FDCPA) you have powerful legal rights:

Right to Validation You can demand written proof that the debt is valid and that Portfolio Recovery Associates has the legal right to collect it.

Right to Dispute If you believe the debt is not yours or the amount is wrong you can dispute it in writing. They must investigate and stop collection activity during the investigation.

Right to Stop Contact You can send a written cease and desist letter demanding they stop all contact. After receiving it they can only contact you to confirm they are stopping communication or to notify you of specific legal action.

Right to Sue If Portfolio Recovery Associates violates the FDCPA you can sue them in federal court for up to $1,000 in statutory damages plus actual damages and attorney fees.

Right to Report You can file complaints against them with:

- The Consumer Financial Protection Bureau (CFPB) at consumerfinance.gov

- The Federal Trade Commission (FTC) at ftc.gov

- Your state attorney general’s office

Step by Step Action Plan — What to Do Right Now

Here is exactly what to do if Portfolio Recovery Associates has contacted you:

Step 1 — Do Not Panic

This is a stressful situation but it is manageable. Millions of Americans deal with debt collectors every year and come out fine.

Step 2 — Do Not Make Any Payment Yet

Wait until you have verified the debt, checked the statute of limitations and understood your options.

Step 3 — Pull Your Credit Report

Go to annualcreditreport.com and pull all three reports for free. Find the Portfolio Recovery Associates entry and note all details.

Step 4 — Check the Statute of Limitations

Find out when you last made a payment on this account and look up your state’s statute of limitations on debt collection.

Step 5 — Send a Debt Validation Request

If it has been less than 30 days since their first contact send a written debt validation request via certified mail.

Step 6 — Decide Your Strategy

| Your Situation | Recommended Strategy |

|---|---|

| Debt is time-barred | Send cease and desist letter, do not pay |

| Debt is valid and recent | Negotiate settlement, request pay for delete |

| You received a lawsuit | Contact consumer rights attorney immediately |

| Debt is not yours | Dispute in writing immediately |

| You want to rebuild credit | Negotiate pay for delete before paying |

Step 7 — Get Everything in Writing

Whatever agreement you reach with Portfolio Recovery Associates get it in writing before making any payment. Verbal agreements are worth nothing.

Step 8 — Consider Professional Help

If you are overwhelmed a nonprofit credit counseling agency or consumer rights attorney can help you navigate this for free or very low cost.

Frequently Asked Questions About Portfolio Recovery Associates

Is Portfolio Recovery Associates a scam?

No. Portfolio Recovery Associates LLC is a legitimate debt collection company regulated by federal law. However they have faced legal penalties for past violations so knowing your rights when dealing with them is essential.

Can Portfolio Recovery Associates garnish my wages?

Yes but only if they win a court judgment against you first. They cannot garnish your wages without suing you and winning. If you respond to any lawsuit they file and raise proper defenses this outcome is not guaranteed.

Will paying Portfolio Recovery Associates improve my credit score?

Not automatically. Paying a collection account updates its status to “paid” but the collection entry remains on your credit report for 7 years. The best outcome for your credit is negotiating a pay for delete agreement where they remove the entry entirely.

How do I get Portfolio Recovery Associates to stop calling?

Send a written cease and desist letter via certified mail. Under the FDCPA they must stop all collection contact after receiving it. Keep your proof of mailing.

Can I negotiate with Portfolio Recovery Associates?

Absolutely. Since they purchased your debt for a fraction of its value they have significant room to settle. Many consumers successfully settle for 25 to 50 cents on the dollar. Never accept their first offer and always get the final agreement in writing before paying.

What if Portfolio Recovery Associates cannot validate my debt?

If they cannot provide proper documentation of your debt within the required timeframe they must stop all collection activity. You can also dispute the debt with the three major credit bureaus — Experian, Equifax and TransUnion — to have it removed from your credit report.

The Bottom Line

Dealing with Portfolio Recovery Associates is stressful, but you have more power in this situation than you probably realize.

Before paying anything:

- Verify the debt is actually yours

- Check whether it is past the statute of limitations

- Request written debt validation

- Understand your credit report options

- Negotiate a settlement or pay for delete agreement

Should you pay Portfolio Recovery Associates? Sometimes yes, when the debt is valid, recent and properly documented. But never pay blindly without understanding your rights and options first.

The consumers who come out best are the ones who stay calm, do their research and respond strategically rather than paying out of fear or ignoring the problem entirely.

You have legal rights. Use them.