Is Accredited Debt Relief Legit? Complete 2026 Review Based on My Analysis

By M. Rizwan Shahid | Personal Finance Coach | Last Updated: May 20, 2026

When you are carrying $15,000, $20,000 or even $30,000 in credit card debt and you feel like you are drowning, the idea of a company that can negotiate your debt down by 45% sounds almost too good to be true.

That is exactly why so many Americans type “is Accredited Debt Relief legit” into Google before picking up the phone to call them.

I spent over a week researching Accredited Debt Relief for this review. I went through their Better Business Bureau profile, reviewed public CFPB complaint data, read through hundreds of real customer reviews on Trustpilot and dug into the fine print of their fee structure that most review sites gloss over.

Here is my completely honest answer, along with everything you need to know before you make any decision about your debt.

What Is Accredited Debt Relief?

Founded in 2011 as a division of Beyond Finance, LLC, Accredited Debt Relief has 15 years of experience and reports helping over 1 million clients with a team of 2,000+ employees across 30 states.

Accredited Debt Relief is a debt settlement company, not a nonprofit, not a bank and not a government agency. They are a for-profit business that negotiates with your creditors on your behalf to reduce the total amount you owe.

Accredited Debt Relief is a BBB-accredited debt relief company offering debt settlement and debt consolidation services. Under the debt settlement program, Accredited Debt Relief’s representatives attempt to negotiate with your creditors to reduce your debt, reportedly by as much as 45 percent.

Before I go any further I want to be direct about something important: debt settlement is a specific financial strategy with real risks and real costs. Whether Accredited Debt Relief is legit is only the first question. The more important question is whether debt settlement itself is the right strategy for your situation, and that depends entirely on your specific circumstances as each case is different from the other.

Is Accredited Debt Relief Legitimate?

The short answer is yes, Accredited Debt Relief is a legitimate company.

Here is the evidence that confirms their legitimacy:

BBB Rating and Accreditation

BBB: A+ rating and BBB accreditation. Public customer reviews are around 4.9 out of 5.

Accredited Debt Relief holds an A+ rating with the Better Business Bureau, the highest available, and is an accredited member of the Association for Consumer Debt Relief, requiring adherence to ethical business practices.

An A+ BBB rating does not mean a company is perfect. It means they have been in business for a sufficient period, they respond to complaints and they meet specific standards for transparency and business practices.

No Unresolved Federal Complaints

According to third-party research, the company has no unresolved FTC or CFPB complaints. The fee structure is transparent, 25% of enrolled debt, success-based only, with no upfront costs.

This is a meaningful distinction. Many debt settlement companies have active CFPB enforcement actions against them. Accredited Debt Relief does not, at the time this review was published.

Industry Accreditation

Industry accreditation: Association for Consumer Debt Relief (ACDR), as referenced in Forbes’ 2026 review.

ACDR membership requires companies to follow a code of ethics that includes fee transparency, honest marketing and proper handling of client funds.

Customer Reviews

Trustpilot: Around 4.8 out of 5 with more than 10,000 reviews.

Accredited Debt Relief has a 4.9 out of 5-star rating on Trustpilot based on more than 4,175 reviews. According to the site, 89% of people rated Accredited Debt Relief as “Excellent,” 9% rated it as “Great” or “Average” and less than 3% rated it “Poor” or “Bad”.

These are strong customer satisfaction numbers by any measure. For context, most financial services companies struggle to maintain a 4.0 rating on Trustpilot.

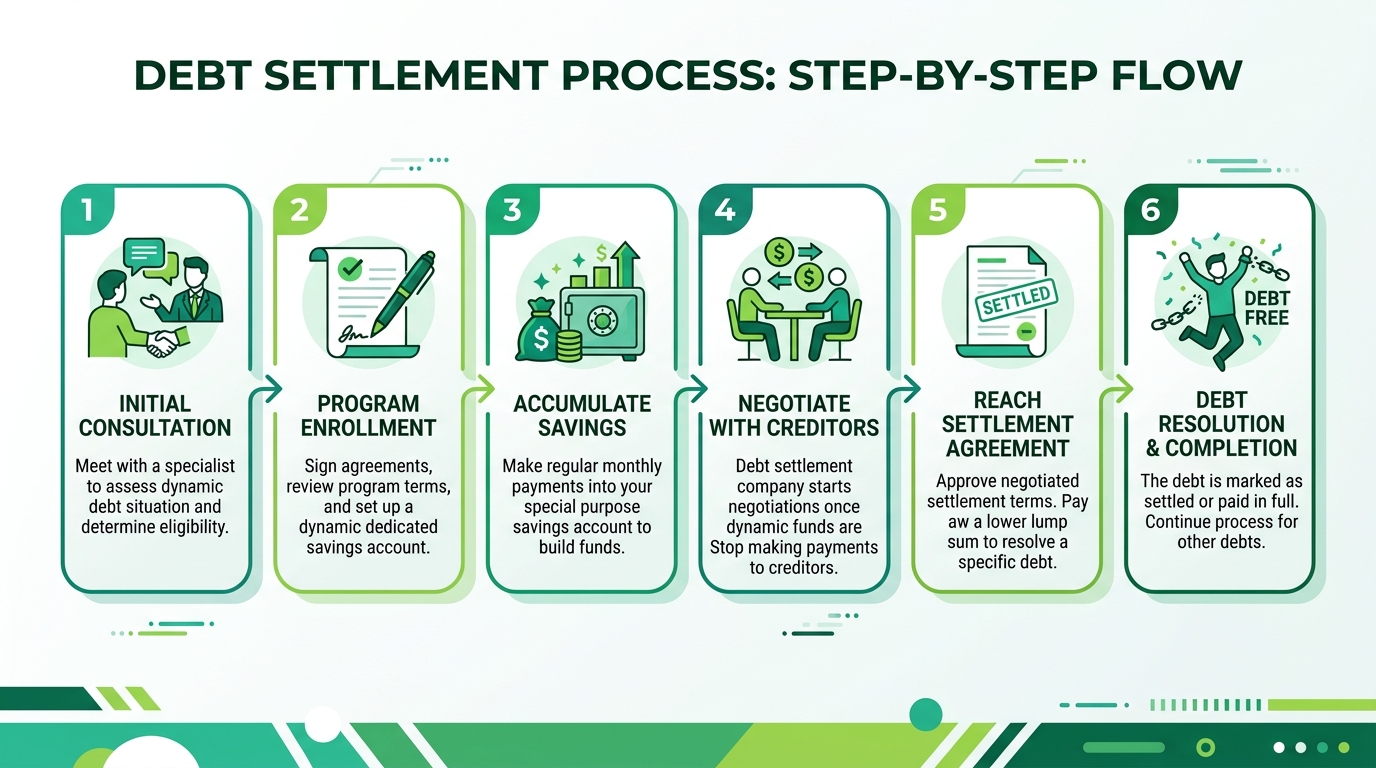

How Does Accredited Debt Relief Actually Work?

Understanding exactly how the program works is essential before making any decision. Most people who are unhappy with debt settlement companies are unhappy because they did not fully understand what they were signing up for.

Step 1 | Free Consultation

The process starts with a free phone consultation. A representative reviews your financial situation, your debts, income, monthly expenses and financial hardship, and determines whether you qualify for their program.

Minimum debt required: $10,000. Time frame: 24 to 48 months. Fees: usually 25 percent of the enrolled debt.

If you have less than $10,000 in unsecured debt Accredited Debt Relief will not be able to help you through their settlement program. This minimum requirement is important to understand upfront.

Step 2 | You Stop Paying Creditors

This is the step that most people are not emotionally prepared for, and the one that causes the most stress during the program.

Accredited Debt Relief works by having you stop payments to creditors and deposit money into a dedicated savings account. As funds accumulate, representatives negotiate with creditors to settle debts for less than you owe.

When you stop making payments your accounts become delinquent. Late fees accumulate. Your credit score drops, often by 100 points or more. Creditors will call you. Some may threaten legal action.

This is not a bug in the debt settlement process. It is how the process works. Creditors are more willing to negotiate reduced settlements when accounts are significantly delinquent because the alternative, collecting nothing, is worse for them.

You need to be mentally prepared for this phase before enrolling. If you are not ready to handle collection calls and credit score decline during the program you should explore other options first.

Step 3 | Monthly Deposits Into Escrow

Instead of sending payments to your creditors you make monthly deposits into a dedicated savings account that you control. This account accumulates over time until there is enough money for Accredited Debt Relief to begin negotiating settlements.

Holds A+ BBB accreditation and is an Association for Consumer Debt Relief member. Charges no upfront costs or monthly fees. Success-based fee of 25% of enrolled debt, not settled amount, is paid only after successful negotiation. Fee is clearly disclosed and deducted from your settlement account when your creditor is paid.

This FDIC-insured account is yours, not the company’s. You can withdraw your money if you decide to leave the program.

Step 4 | Negotiation and Settlement

Once sufficient funds have accumulated Accredited Debt Relief begins negotiating with each creditor individually. They aim to settle each account for less than the full balance owed.

Accredited Debt Relief says that its clients repay on average 55% of their debt balances and usually a 25% settlement fee.

This means on average clients pay 55 cents on the dollar of their enrolled debt, plus the 25% company fee on top of that.

Step 5 | Settlement and Fees

Accredited Debt Relief typically charges 25 percent of the enrolled debt. This means you will pay based on the amount of debt you enroll with the company rather than the amount settled.

This distinction matters enormously. The fee is calculated on what you enrolled, not what you settle for.

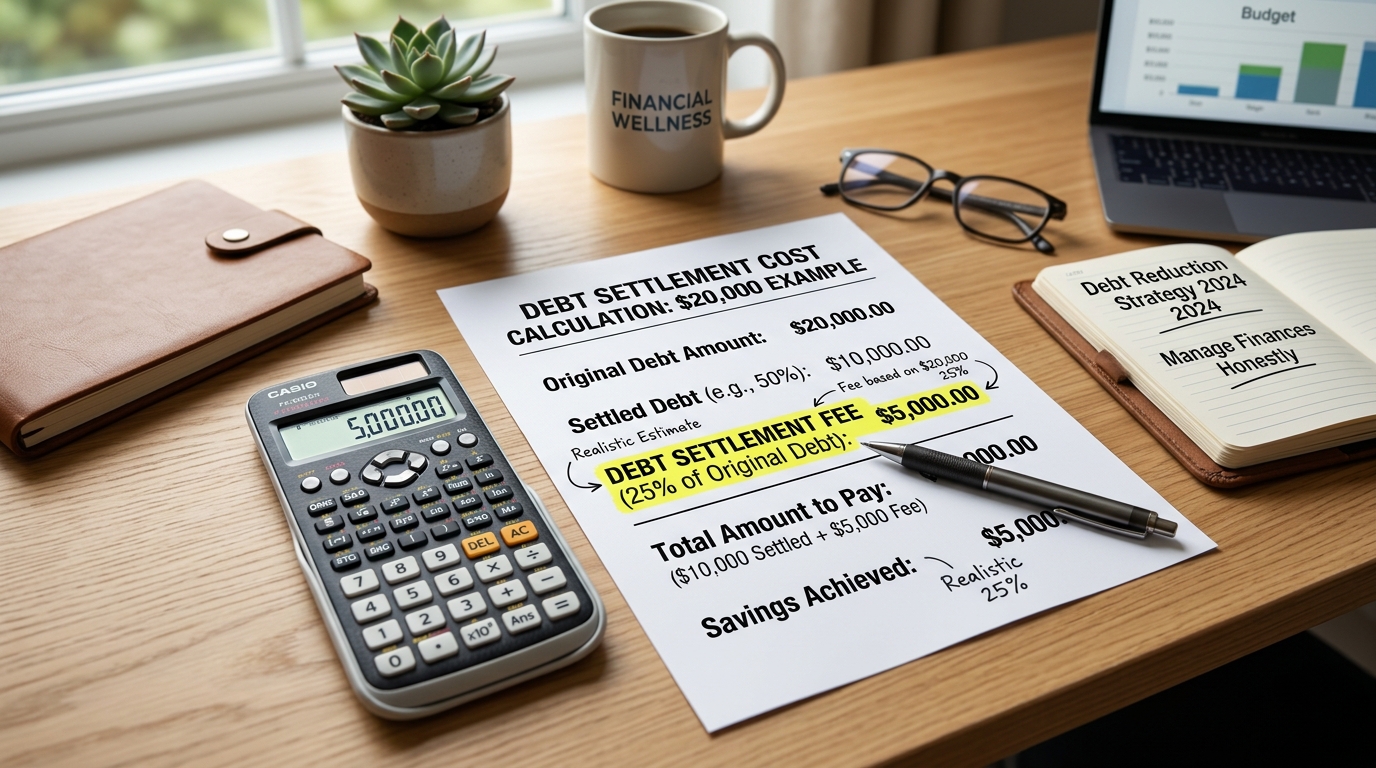

Here is a real example. If you enroll $20,000 in debt:

| Item | Amount |

|---|---|

| Original debt enrolled | $20,000 |

| Settlement amount (55% avg) | $11,000 |

| Accredited Debt Relief fee (25% of enrolled) | $5,000 |

| Total you actually pay | $16,000 |

| Total saved vs original debt | $4,000 |

On $20,000 in debt the average client saves approximately $4,000 after fees. That is real savings, but it is not the “45% reduction” that the headline numbers might suggest once fees are factored in.

What Are the Real Fees?

Accredited Debt Relief operates as a division of Beyond Finance and is one of the top debt solution companies in the country. Rates are typically 25%. There’s no guarantee your creditors will agree to settle for less than you owe.

Someone coming to Accredited Debt Relief with $20,000 of credit card debt, for example, would pay about $5,000 to Accredited Debt Relief when that debt is settled.

There are also potential hidden costs that the company does not prominently advertise:

Taxes on forgiven debt. Under IRS rules debt that is forgiven or cancelled is typically treated as taxable income. If you settle a $10,000 debt for $5,000 the $5,000 that was forgiven may be reported to the IRS as income on a Form 1099-C. You could owe federal and state income taxes on that amount.

Your creditors may continue to add late fees and penalties to your accounts if you stop paying on those accounts while attempting a settlement, which is common practice when negotiating debt settlements.

Creditor legal action. While your accounts are delinquent creditors retain the right to sue you. Accredited Debt Relief does not guarantee that creditors will negotiate rather than sue. Most creditors do prefer to negotiate, but it is not guaranteed.

What Types of Debt Does Accredited Debt Relief Handle?

Accredited Debt Relief only works with unsecured debt. Each service is tailored to your personal situation and financial goals.

Accredited Debt Relief explicitly promotes assisting with the following types of debt: credit card debt, department store credit debt, medical debt and personal loan debt.

They do NOT settle:

- Mortgages or home equity loans

- Auto loans

- Federal student loans

- Child support or alimony

- Tax debt

- Business debt secured by collateral

Who Qualifies for Accredited Debt Relief?

You will need at least $10,000 in eligible debt to qualify for Accredited.

Accredited Debt Relief is available in 37 U.S. states.

Accredited Debt Relief does not have a minimum credit score requirement for the debt settlement program. However, it may have a minimum requirement for debt consolidation loans.

The ideal candidate for Accredited Debt Relief is someone who:

- Has at least $10,000 in unsecured debt, credit cards, medical bills or personal loans

- Is experiencing genuine financial hardship and struggling to make minimum payments

- Lives in one of the 37 states where they operate

- Has stable enough income to make consistent monthly deposits into the escrow account

- Is seriously considering bankruptcy as the alternative and wants to explore settlement first

- Understands and accepts the credit score impact during the program

If you can comfortably make your minimum payments every month debt settlement is almost certainly not the right tool for your situation. Debt settlement is designed for people in genuine financial distress.

What Do Real Customers Say?

I read through hundreds of verified customer reviews to find the patterns that matter — not just the five-star praise or the one-star rage.

What Happy Customers Report

Many online reviews express appreciation for a positive experience with Accredited Debt Relief. Most reviewers report interacting with knowledgeable representatives who can explain debt relief options with patience and empathy.

The most consistent positives across verified reviews are:

Helpful and patient consultation process. Multiple reviewers specifically mention that the initial consultation felt informative and non-pressured, they were given real information about the program before being asked to enroll.

Responsive customer service. Customer support is available by phone and email seven days a week. Many reviewers note that representatives were accessible and responsive throughout the program.

The program worked as described. Reviewers who completed the program and settled their debts consistently report that the outcomes matched what they were told to expect during enrollment.

Online dashboard and mobile app. Mobile app on iOS and Android and online dashboard provide 24/7 access to track progress and communicate with support. Reviewers appreciate the transparency this provides during what can be a long and stressful process.

What Unhappy Customers Report

The most common complaint against Accredited Debt Relief in online reviews is excessive follow-up after the initial consultation. Several consumers who inquired about the service and decided against it were contacted multiple times after expressing disinterest.

Additional complaints from negative reviews include:

The process takes longer than expected. As you will find with any debt settlement company there are a few negative reviews about how long the process takes and/or the lack of progress. As a reminder, debt settlement can take 24 to 48 months and some creditors may refuse to settle despite all efforts from the debt relief company.

Credit score damage was more severe than anticipated. Some reviewers express surprise at how significantly their credit score dropped during the program, despite this being disclosed upfront. If you have never experienced serious credit damage the psychological impact can be more difficult than the financial reality.

Not all creditors agreed to settle. Some reviewers report that specific creditors refused to negotiate, leaving those accounts unresolved at the end of the program.

Fee structure felt expensive in hindsight. After completing the program some clients felt that the 25% fee reduced their actual savings more than they had anticipated during enrollment. This underscores the importance of running the real math before signing up.

My Assessment of the Reviews

The pattern that emerges from reviewing hundreds of real customer accounts is this: Accredited Debt Relief delivers what it promises for most clients who qualify and complete the program. The dissatisfied customers are typically those who either did not fully understand the process before enrolling or were not ideal candidates for debt settlement in the first place.

This is not a defense of the company. It is a realistic assessment that helps you determine whether this is the right tool for your situation.

Accredited Debt Relief vs Alternatives | What Should You Actually Do?

This is the most important section of this entire review. Accredited Debt Relief may be legitimate, but that does not mean it is the right choice for you. Here is an honest comparison of your real options.

Option 1 | Nonprofit Credit Counseling (Best for Most People)

If you can make your minimum payments but are struggling with high interest rates a nonprofit Debt Management Plan through an agency affiliated with the National Foundation for Credit Counseling is almost always a better choice than debt settlement.

You pay your full balance at reduced interest rates, typically 6% to 9% instead of 20%+, over 3 to 5 years. Your credit is not damaged. No creditor lawsuits. Fees are minimal, usually $25 to $50 per month. And you pay back everything you borrowed.

Choose this if: You can make your minimum payments and your problem is high interest rates not an unmanageable total balance.

Option 2 | DIY Debt Negotiation

If your accounts are already significantly delinquent you can negotiate directly with creditors yourself without paying a company 25% of your enrolled debt.

Creditors negotiate with consumers directly every day. They will often accept settlements of 40% to 60% of the balance, similar to what Accredited Debt Relief achieves, without the company fee. This requires time, persistence and a willingness to handle uncomfortable phone calls. But it can save you thousands of dollars in fees.

Choose this if: You have the time and emotional energy to handle the negotiation process yourself.

Option 3 | Accredited Debt Relief or Similar Debt Settlement

Debt settlement through a company like Accredited Debt Relief makes sense when you have significant unsecured debt, $10,000 or more, you are genuinely unable to make minimum payments and you want professional help navigating the process without doing it alone.

Choose this if: You have $10,000 or more in unsecured debt, you are genuinely struggling to make minimum payments and you want structured professional support.

Option 4 | Bankruptcy

For people with overwhelming debt and no realistic path to repayment bankruptcy provides legal protection and a structured fresh start. Chapter 7 eliminates most unsecured debt. Chapter 13 creates a court-supervised repayment plan.

Bankruptcy has serious long-term credit implications, it stays on your report for 7 to 10 years, but it is a legitimate legal tool designed exactly for situations of genuine financial crisis.

Choose this if: Your total debt genuinely exceeds your ability to repay even over a 3 to 5 year period.

The Federal Trade Commission provides an excellent free overview of all debt relief options with no sales pressure. I strongly recommend reading it before making any decision.

The Hidden Cost Nobody Talks About | Taxes on Forgiven Debt

I want to spend extra time on this because it is the cost that surprises debt settlement clients most consistently.

Under IRS rules on cancellation of debt, when a creditor forgives part of what you owe them that forgiven amount is typically treated as taxable income in the year it is settled.

Here is how this plays out in real numbers. You enroll $20,000 in credit card debt. Accredited Debt Relief negotiates a settlement of $11,000, meaning $9,000 is forgiven. The creditor sends you and the IRS a Form 1099-C for $9,000.

If you are in the 22% federal tax bracket you could owe approximately $1,980 in federal income tax on that $9,000 of forgiven debt, on top of the $5,000 company fee you already paid.

There is an important exception. If you are technically insolvent at the time of settlement, meaning your total debts exceed your total assets, you may qualify for the IRS insolvency exemption and owe no taxes on the forgiven amount. Most clients in genuine financial distress do qualify for this exemption. But you need to work with a tax professional to document your insolvency position correctly.

Always consult a tax professional before enrolling in any debt settlement program. Understanding your tax situation is part of calculating your true total cost.

Step by Step | What to Do Before Calling Accredited Debt Relief

Before you dial their number run through this checklist. The answers will determine whether debt settlement is actually appropriate for your situation.

Step 1 | Calculate Your Total Unsecured Debt

List every unsecured account, credit cards, medical bills, personal loans, store cards. Add up the total. If it is under $10,000 Accredited Debt Relief cannot help you with their primary program.

Step 2 | Pull Your Free Credit Report

Go to annualcreditreport.com, the federally authorized free credit report site, and pull all three reports. Understand what is currently on your report and what collection accounts are already affecting your score.

Step 3 | Talk to a Nonprofit Credit Counselor First

Contact the National Foundation for Credit Counseling for a free or low-cost consultation with a certified credit counselor. They have no financial incentive to push you toward any specific solution. They will give you an honest assessment of all your options.

This one step could save you thousands of dollars if it turns out a Debt Management Plan works better for your situation than debt settlement.

Step 4 | Run the Real Numbers on Debt Settlement

If debt settlement does appear to be the right path use this formula to understand your actual savings before enrolling with anyone:

Your enrolled debt × 55% (average settlement rate) = Settlement amount you pay to creditors

Your enrolled debt × 25% (Accredited’s fee) = Fee you pay to Accredited Debt Relief

Settlement amount + Fee + Estimated tax on forgiven debt = Your true total cost

Compare that total cost to your original debt and to what continued minimum payments would cost you over the next 5 to 10 years.

Step 5 | Verify They Operate in Your State

Visit accrediteddebtrelief.com/state and confirm they are licensed to operate in your specific state. They are currently available in 37 states. If your state is not on the list you will need to find a licensed alternative.

Step 6 | Check the CFPB Complaint Database

Search for Accredited Debt Relief directly in the CFPB public complaint database. Review any complaints for patterns, what the complaints are about matters more than how many there are. A company serving over one million clients will have some complaints. The question is whether those complaints reveal systemic problems.

Frequently Asked Questions About Accredited Debt Relief

Is Accredited Debt Relief a scam?

No. Accredited Debt Relief is a legitimate debt settlement company with 15 years of operation since 2011 and over 1 million clients served. The company holds an A+ rating with the Better Business Bureau, the highest available, and is an accredited member of the Association for Consumer Debt Relief, requiring adherence to ethical business practices. If you receive any communication claiming to be from Accredited Debt Relief through Facebook Messenger, WhatsApp or Telegram it is a scam, the real company has publicly stated they will never contact clients through those channels.

How much does Accredited Debt Relief charge?

Accredited Debt Relief typically charges 25 percent of the enrolled debt. This means you will pay based on the amount of debt you enroll with the company rather than the amount settled. Accredited Debt Relief does not charge any upfront fees for debt settlement. Fees are performance-based and contingent upon reaching a favorable settlement with creditors.

What is the minimum debt to use Accredited Debt Relief?

In order to be eligible for Accredited Debt Relief’s services you must have at least $10,000 in unsecured debt. This barrier to entry limits the choices of those with lesser debt amounts who are seeking debt relief.

How long does the Accredited Debt Relief program take?

The time frame for Accredited Debt Relief’s program is 24 to 48 months depending on your total enrolled debt, the number of creditors involved and how quickly those creditors agree to negotiate.

Will Accredited Debt Relief hurt my credit score?

Yes, significantly. When you stop making payments to creditors as part of the debt settlement process your accounts become delinquent and your credit score will drop, often by 100 points or more. Like all debt settlement programs, clients typically experience significant credit score damage of 100+ points and may face creditor lawsuits. This credit damage is a real cost of the program that must be weighed against the potential savings.

Is the debt forgiven by Accredited Debt Relief taxable?

Potentially yes. Under IRS rules forgiven debt is typically considered taxable income in the year it is settled. However many debt settlement clients qualify for the IRS insolvency exemption. Consult a tax professional about your specific situation before enrolling. The IRS publication on cancellation of debt explains the rules in full detail.

What states is Accredited Debt Relief available in?

Accredited Debt Relief is available in 37 U.S. states. Check their official state page at accrediteddebtrelief.com/state to confirm availability in your specific state before beginning the consultation process.

What happens if my creditors refuse to settle?

There is no guarantee your creditors will agree to settle for less than you owe. If a creditor refuses to negotiate Accredited Debt Relief continues to work on other enrolled accounts. The funds accumulated for that specific creditor remain in your account. You can use those funds toward the balance, find a different resolution or in some cases creditors may eventually become more willing to negotiate as the account ages further.

My Honest Verdict

After a week of research, reviewing their BBB profile, reading the CFPB complaint database, going through hundreds of verified customer reviews and analyzing their complete fee structure, here is my honest conclusion about Accredited Debt Relief in 2026.

Accredited Debt Relief is legitimate. They are a real company with real credentials, a genuine track record and strong customer satisfaction ratings. They deliver what they promise for most clients who qualify and complete the program.

But legitimate is not the same as right for everyone.

Debt settlement is an expensive, credit-damaging, multi-year process that makes sense in a specific and relatively narrow set of circumstances, when you have significant unsecured debt, you are in genuine financial hardship and you have explored less damaging alternatives first.

If you are in that situation, if you have $10,000 or more in unsecured debt, you are genuinely unable to make your minimum payments and you have already explored nonprofit credit counseling, then Accredited Debt Relief is one of the more reputable options available to you in 2026.

If you are not in that situation, if you can make your payments but are stressed about high interest rates, or if your debt is under $10,000, there are better tools for your situation that will cost you less and do less damage to your credit.

Before making any decision consult a certified nonprofit credit counselor at NFCC.org. It is free, unbiased and could save you thousands of dollars by pointing you toward the most appropriate solution for your specific circumstances.

Whatever path you choose, building a solid financial foundation is the ultimate goal. Our get out of debt guides cover every aspect of debt payoff from handling individual collection accounts to understanding debt settlement and rebuilding your credit after financial hardship. Our budgeting resources and save money guides give you the complete framework for building financial stability that lasts.

Rich Beginners Editorial Standards: This review was researched and written by M. Rizwan Shahid, a certified financial wellness coach with 8 years of experience helping Americans navigate debt and financial recovery. All facts have been verified against primary sources including the Better Business Bureau, Consumer Financial Protection Bureau, Federal Trade Commission and the company’s official disclosures. This article was last updated May 20, 2026. Rich Beginners is not affiliated with Accredited Debt Relief and receives no compensation for this review. Read our full editorial policy.

M.Rizwan Shahid is a personal finance writer and certified financial wellness coach with over 8 years of experience helping Americans navigate debt, credit rebuilding and budgeting on tight incomes. After personally paying off $23,000 in credit card debt using the strategies covered on this site, Rizwan now helps everyday Americans do the same. His work has been cited by financial educators and consumer advocacy groups across the USA.